Одноразовые медицинские маски

О нас

ЧПТУП «Дом моды Тамара» — белорусский производитель одноразовых медицинских масок. Основным направлением деятельности организации является производство и оптовая продажа одноразовых масок SMS. Маски имеют трехслойную структуру и состоят из нетканых материалов: спанбонд S, мельтблаун M, спанбонд S.

Использование фильтрующего слоя мельтблаун делает наши маски действительно качественными. Этот уникальный нетканый материал обеспечивает хорошую воздухопроницаемость и бактериальную фильтрацию не менее 98%, что подтверждено протоколом испытаний в Республике Беларусь.

Сфера применения одноразовых медицинских масок

Одноразовая маска — универсальное средство защиты органов дыхания от факторов, которые передаются водушно-капельным путем:

- возбудителей грибковой, бактериальной, вирусной пневмонии;

- всевозможных аллергенов;

- опасных испарений;

- биологических жидкостей;

- аэрозолей;

- пыли и прочих твердых частиц, которые находятся в воздухе во взвешенном состоянии.

Защитные медицинские маски

- стоят недорого, при этом обладают высокой степенью защиты;

- рекомендованы для поддержания высокого санитарно-гигиенического уровня не только медикам, но и населению, особенно в период пандемии;

- позволяют сдержать распространение инфекции, защитить себя и своих близких от возможного заражения;

- мало весят и практически не затрудняют дыхание;

- не давят, не натирают, не вызывают раздражения или аллергии;

- используются в течение 2-3 часов, после чего выбрасываются и заменяются новыми.

Почему выбирают нас

Сроки

Поставки товара осуществляются нами в кратчайшие сроки благодаря использованию новейшего оборудования и тщательно проработанной логистической системе

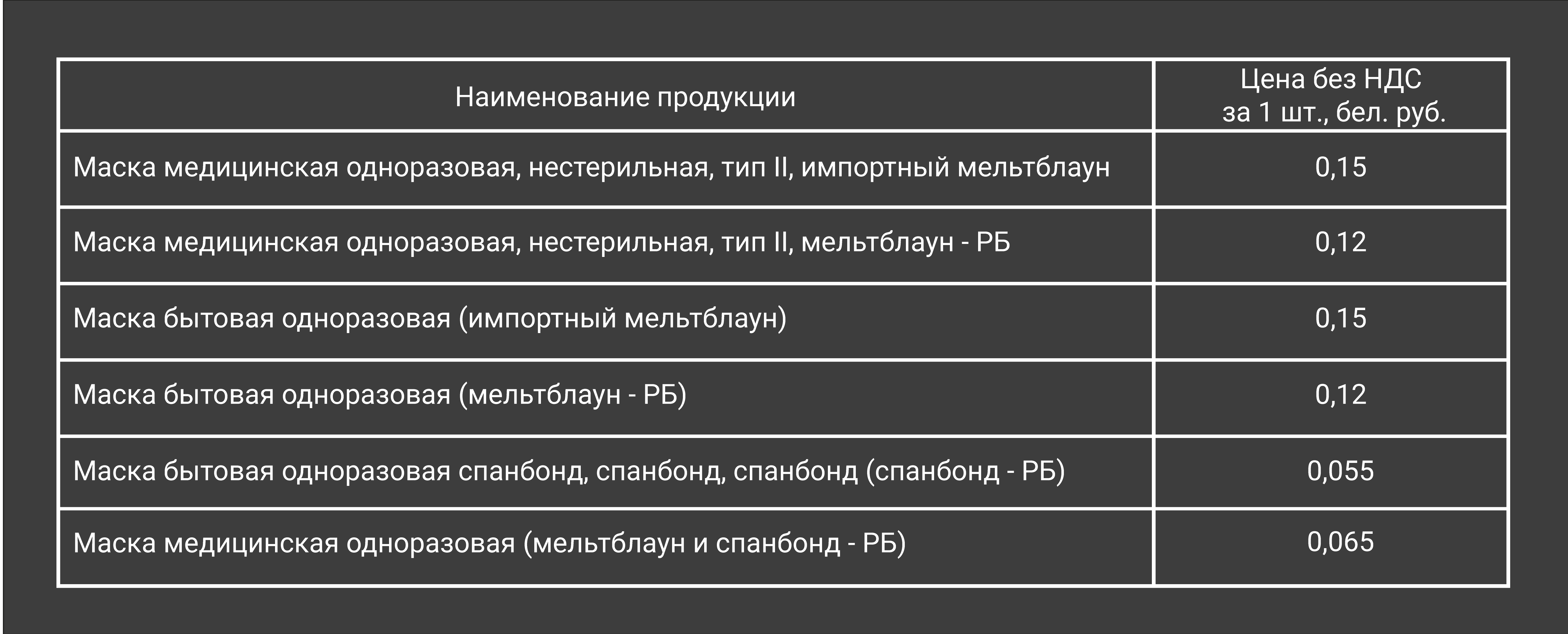

Цена

Для каждого клиента гарантирован индивидуальный подход и гибкая ценовая политика

Качество

Используем только современные материалы и технологии, которые гарантируют качество выпускаемой продукции

Собственное производство

Мы поставляем только собственно произведенный белорусский товар, тем самым можем гарантировать неизменное качество с течением времени

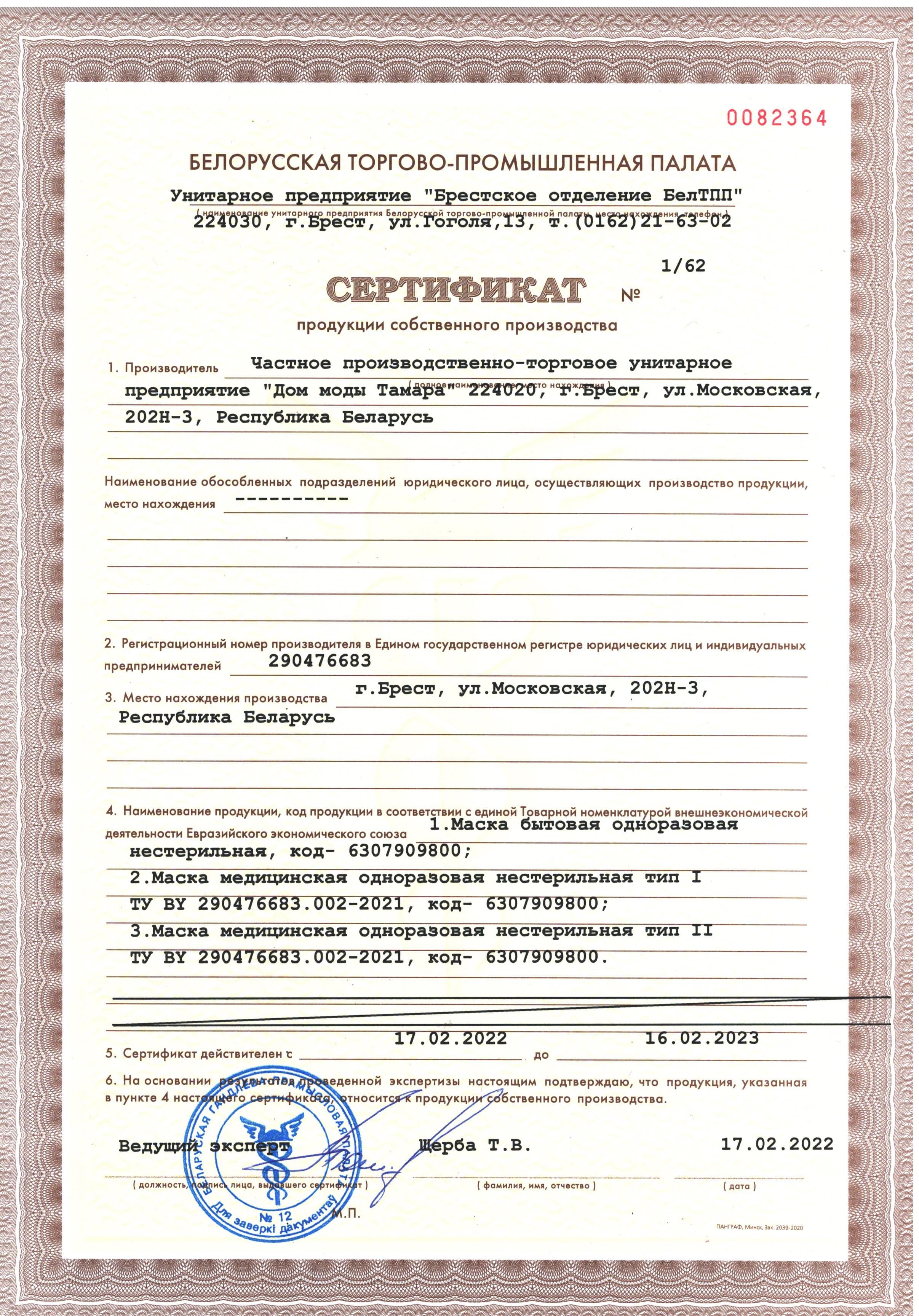

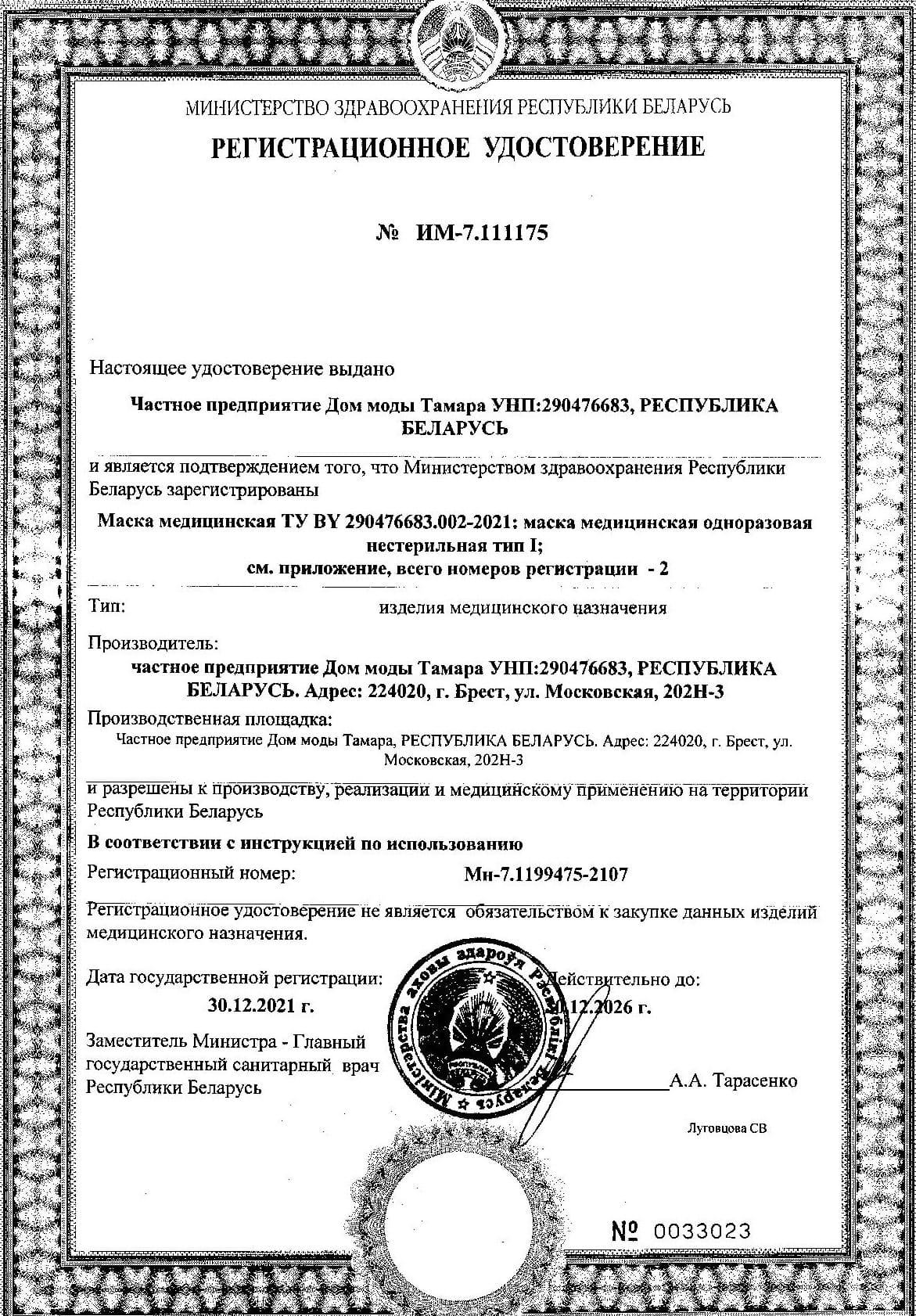

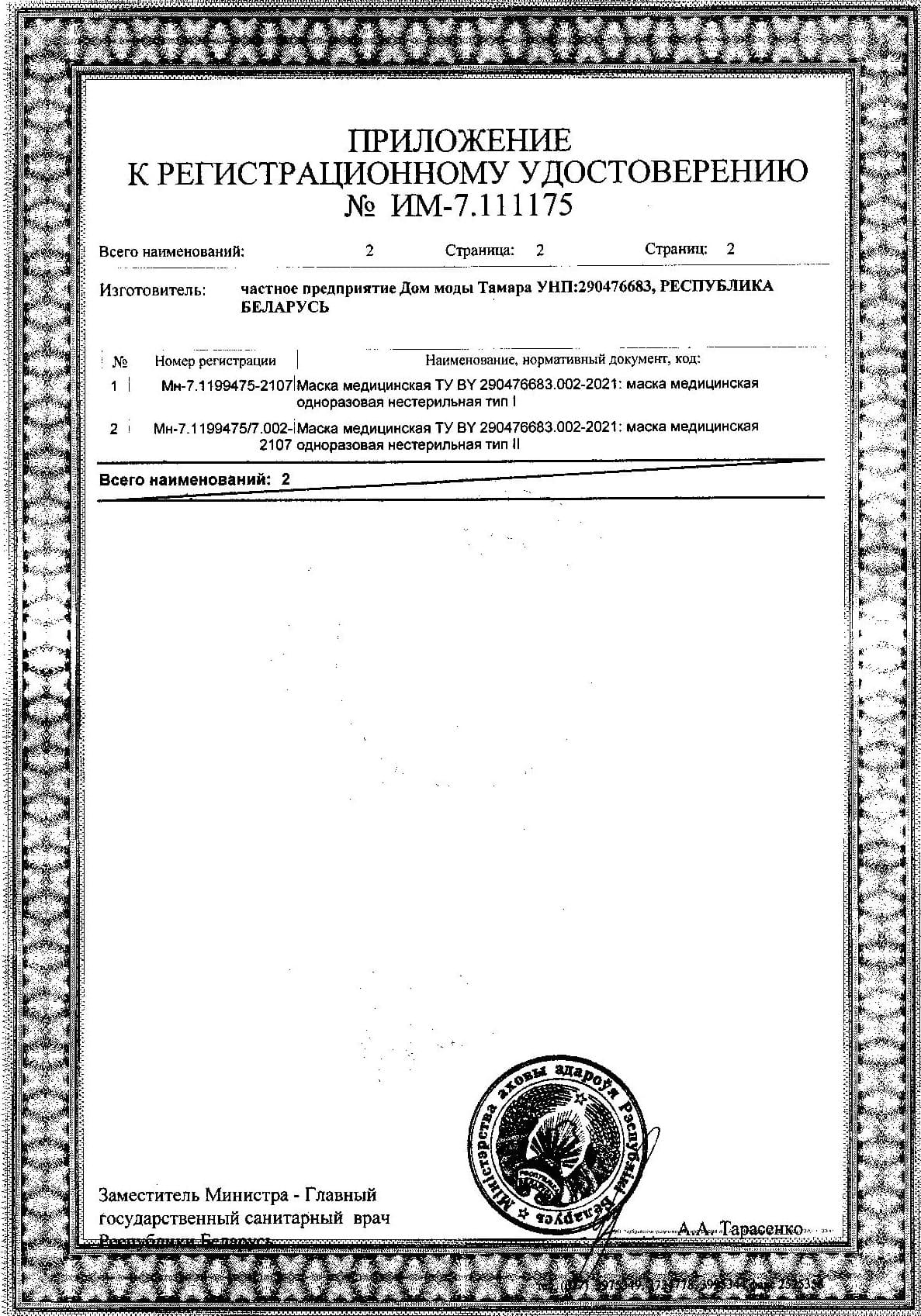

Сертификаты соответствия